Featured

Table of Contents

While brand-new credit can assist you restore, it is essential to room out your applications. If you have a member of the family or close friend with outstanding credit report, take into consideration asking to add you as an authorized individual on one of their charge card. If they do it, the complete background of the account will certainly be added to your credit rating reports.

Before you consider debt negotiation or bankruptcy, it's crucial to recognize the potential advantages and negative aspects and just how they might apply to your circumstance. Both choices can lower or get rid of large portions of unsafe financial obligation, helping you prevent years of unmanageable settlements.

If you're not exactly sure that debt negotiation or personal bankruptcy is appropriate for you, right here are a few other financial debt alleviation alternatives to consider. The appropriate method will certainly depend on your situation and goals. If you have some versatility with your spending plan, here are some sped up financial debt settlement alternatives you can seek: Beginning by noting your financial debts from the smallest to the biggest balance.

The 9-Second Trick For Questions to Ask a Debt Relief Provider

The therapist discusses with creditors to lower rates of interest, waive late costs, and produce a workable regular monthly repayment. You make one consolidated repayment to the firm, which after that pays your monetary institutions. While a DMP does not lower the principal balance, it aids you settle financial debt much faster and a lot more economically, commonly within three to 5 years.

While you can negotiate with lenders by yourself, it's commonly a difficult and taxing process, specifically if you need to resolve a big quantity of debt across a number of accounts. The process requires a solid understanding of your finances and the financial institution's terms along with self-confidence and persistence. For this reason, there are financial debt alleviation business also recognized as financial debt negotiation business that can deal with the negotiations for you.

People who sign up in financial debt alleviation programs have, typically, roughly $28,000 of unsafe financial obligation throughout almost 7 accounts, according to an evaluation commissioned by the American Association for Debt Resolution, which checked out clients of 10 significant financial obligation alleviation firms between 2011 and 2020. Regarding three-quarters of those clients had at the very least one debt account successfully worked out, with the normal enrollee clearing up 3.8 accounts and more than half of their enrolled financial obligation.

It prevails for your credit report to fall when you first begin the financial debt alleviation procedure, particularly if you stop paying to your financial institutions. As each financial obligation is settled, your credit scores score should begin to rebound. Make sure you comprehend the total prices and the impact on your credit rating when assessing if financial obligation negotiation is the appropriate option.

The Of Immediate Consequences of Personal Credit Rating

As pointed out over, there are choices to financial obligation settlement that might be a far better fit for your monetary situation. Below's a quick break down of how each option functions: Debt loan consolidation allows you incorporate numerous financial debts right into one by getting a new financing to settle your present financial debts. This approach turns several financial obligations right into a single regular monthly repayment and typically offers a lower rate of interest, simplifying your finances and possibly saving you money in time.

Below's how each one works: Financial debt combination loans: These are individual financings that you can make use of to resolve your existing financial debts, leaving you with simply one month-to-month bill, commonly at a lower rate of interest. Balance transfer credit report cards: This includes moving your existing charge card balances to a brand-new credit scores card that offers a lower interest rate or an advertising 0% APR for a set period.

Once the duration ends, rate of interest will certainly be considerably high often over 20%. Home equity finances or HELOCs (home equity credit lines): These loans enable you to obtain against the equity in your home. You get a swelling sum or a credit line that can be utilized to pay off debts, and you typically gain from lower rates of interest compared to unsafe fundings.

Rumored Buzz on Things to Avoid When Researching a Bankruptcy Provider

These plans have several advantages, such as simplifying your repayments by consolidating numerous right into one and possibly reducing your rate of interest. They typically come with a setup charge ranging from $30 to $50, and a monthly upkeep fee of around $20 to $75, depending on the agency you work with.

Having a great deal of debt can be overwhelming, but it's still crucial to put in the time to consider the information of various services so you comprehend any possible risks. The most effective financial obligation prepare for you depends on your monetary scenario. If you're battling with your bills however still haven't missed out on any type of settlements, a financial debt monitoring plan may be a good fit specifically if you do not want your credit rating to tank.

Whichever your circumstance is, consider talking with a licensed credit report therapist, an insolvency attorney, or a qualified debt specialist before relocating onward. They can help you get a full understanding of your funds and choices so you're better prepared to choose. One more element that influences your options is the sort of debt you have.

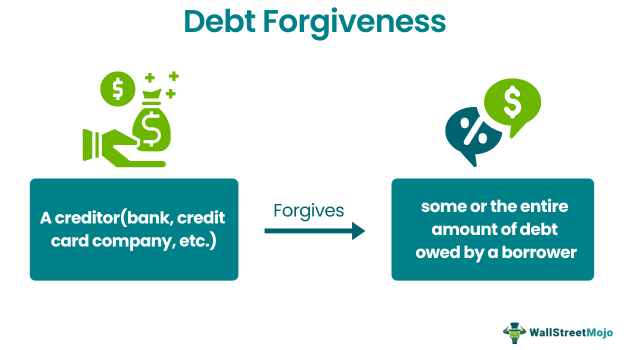

It is important to comprehend that a discharge stands out from financial debt forgiveness, and financial debt does not obtain "forgiven" through a personal bankruptcy declaring. Our West Hand Coastline personal bankruptcy attorneys can discuss in more detail. In basic, "financial obligation mercy" describes a circumstance in which a creditor does not think it can gather the full amount of the financial obligation owed from a debtor, and either quits attempting to gather or agrees to forgive an amount less than what the borrower owed as part of a financial obligation settlement contract.

Little Known Facts About True Stories from Debt Relief Recipients.

When this takes place, the debt will certainly be considered "canceled" by the internal revenue service, and the borrower will generally obtain a termination of financial debt create the quantity of financial debt forgiven is taxable. In an insolvency situation, financial debt is not forgiven by a lender. Instead, it is released by the bankruptcy court, and discharge has a various significance from financial debt mercy.

{kind=link}

Table of Contents

Latest Posts

The Best Strategy To Use For Does Rebuild Credit While Paying Off Medical Loans Make Sense for Everyone

The smart Trick of No-Cost Informational Financial Literacy Resources Offered to You That Nobody is Talking About

Widespread Myths Regarding Debt Forgiveness Fundamentals Explained

More

Latest Posts

The Best Strategy To Use For Does Rebuild Credit While Paying Off Medical Loans Make Sense for Everyone

The smart Trick of No-Cost Informational Financial Literacy Resources Offered to You That Nobody is Talking About

Widespread Myths Regarding Debt Forgiveness Fundamentals Explained